The McCloud judgement declared that the transition of public sector pensions introduced in 2015 was illegal. This explains the relevance to the Teachers’ Pension schemes.

Reflections on reaching for retirement

The McCloud judgement declared that the transition of public sector pensions introduced in 2015 was illegal. This explains the relevance to the Teachers’ Pension schemes.

Pensions are a fraction of your salary. (80th, 60th, 57th etc) so does taking a pension mean having to watch every penny…it’s not as big a cut as you may think.

youTube: Poor Pensioners – Just how big a drop in income is it?

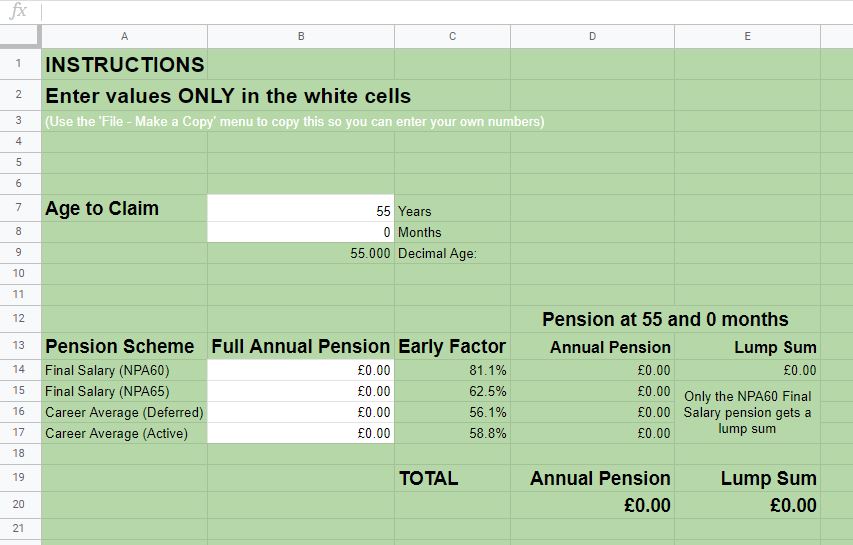

One of the biggest myths, or misunderstandings, is that taking the pension ‘early’, as early as 55, LOSES 20% of your pension.

There is some truth to this figure but it is NOT as significant as it first sounds…I explain more here

He was great! He has plenty of ‘tools’ on his web-site. Plenty of food for thought!. We are now booking in some financial advice!

I thought it was really eye opening and I wish I’d had it earlier in my career – I would have kept every pay slip!

David was fantastic and explained our choices in a clear and concise manner that has given me a much better understanding on how to maximise both <name redacted> and my pension

In my years of teaching since 2009, I have not had anyone talk to me like that and being so frankly honest about something so important involving my future. It was so refreshing. David was very knowledgeable and having a ‘one to one’ with him was great, I only wish I had more time with him. It’s great too that I have his contact details for future reference.

Thanks David from one fellow teacher to another!

All the best

A necessary and invaluable use of time. There may be actions that you did not know that you need to take to make the most of your pension.

Definitely go! You will learn a lot and know some more questions that you need to follow up.

Treat it as if your life depended on it. Or as if David is giving away free money. Because he is!

Made a complicated thing seem less terrifying. As a younger member of staff it gave me reassurance and guidance on what to keep an eye in terms of pension

Very informative and helpful to decode the language and meaning of many confusing aspects of the pension system

Go – hugely important and informative, really really helpful, made me realise I need to get my dates etc in order as there are gaps from early on in my career. .

Proudly powered by WordPress | Theme: Baskerville 2 by Anders Noren.