Your employer is allowed to deny permission for you to take “early” retirement for up to 6 months….is that for real?

There is a rule that says that if you are applying for “early” retirement then your employer has to “agree”.

A first sight the rule appears to be rather punitive, but once you drill down into the detail there is a “get out” clause and it is only when you understand why the rule was conceived in the first place does it even make any sense at all.

Your employer is entitled to withhold their permission for up to 6 months.

However, the “get out” clause is exactly as it sounds. Their denial of permission only lasts for as long as you are employed by them.

Their blocking of your application ends on the very last day of your employment, though you must have given the TPS at least 6 weeks notice.

Regulation 12(3)(b) under Schedule 7 (Case E: early retirement):

(b) where P ceases to be in that employment before 6 months have expired since the date on which P asks P’s employer to agree, such day as P specifies in the application, which must be no earlier than 6 weeks after the date on which P’s application is made.

The rationale for this rule’s inclusion is that the pension scheme is not allowing a teacher to get around their contract of employment and take their pension whilst still “employed”.

A teacher has to give a minimum of 3 months notice to leave their employment and this rule is designed to prevent a teacher walking out of their contract and taking the pension immediately.

So, yes, taking the pension “early” requires you get the permission from your employer, but so long as you ASK for it, and apply for the pension, at least 6 weeks before the end of your employment contract it doesn’t matter if they give or deny you that permission since your pension will be paid on the first day after leaving employment so long as you have given the required notice to resign your employment.

The Pension scheme lays down very clearly how long a break is needed in order to take the pension before you reach you Normal Pension Age:

The Schedule in the regulations that covers taking “Early” retirement starts on page 121 and is called “Case E”

Case E: early retirement with actuarial adjustment 10.—(1) A person (P) falls within this paragraph if— (a) P was in pensionable or excluded employment at any time after 29th March 2000, (b) P ceases to be in such employment,

There are other parts to this regulation but the key part above is that you have to “cease” to be in employment. This is then expanded on to explain what is meant be “ceasing” in regulation 14, shown below:

For the purpose of this Schedule— 14 (a) a person is not to be treated as ceasing to be in pensionable or excluded employment unless at least one day passes without the person being in such employment after the person ceases to be in such employment;

Simply put, you can take the pension early so long as you are not employed as a teacher ON the day you have asked for the pension to begin.

School Policies

Unfortunately many schools and LAs get confused over what is a break in employment, using what is needed to reset other employment rights and not what is needed for an employee to take their pension. There is no legal barrier to an employer ending, with the agreement of the employee, a contract of employment on one day and starting a new contract after a gap of 24 hours.

A number of schools HR departments are rather lazy in this regard and instead of just doing what is required to enable the employee to take their pension insist on a longer break because of their misunderstanding of what is needed to constitute a “break” in employment. This is often based on other employment rights, such as avoiding having to repay redundancy payments, or entitlement to sick pay etc.

Redundancy – The Main Misunderstanding

The most common misunderstanding over a break in service is that policies in schools and authorities have been written to avoid claims of wrongful dismissal or to prevent the invalidation of a redundancy payment. Where BOTH parties are in agreement over the nature and length of a break in employment neither of these concerns apply.

Unfortunately, if they do insist on a longer break there is very little the teacher can do in such circumstances since they are over a barrel as they do need the break in employment in order to start taking the pension before their normal pension age.

Over the Normal Pension Age

Whilst a break in employment would allow a teacher who is over the normal pension age for a scheme (60/65 etc) , it is not the ONLY way such a teacher can trigger the creation and payment of their pension.

They can start payment of their final salary pensions simply by opting out of the pension scheme without needing any break in employment.

Is it illegal to have a day between contracts?

This is the key question to ask HR advisors who are insisting that a longer break is required. The answer, of course, is “no”.

Is it illegal to appoint someone without advertising a post?

Another key question, to which the answer is also “no”

Staffing in Schools

There are guidance and Statutory Instruments (SI) on how staffing in schools should be undertaken, and both of these documents have NO requirement that a break in contracts be of any given minimum length, nor that a post has to be advertised and the member of staff made to reapply for their position.

Even for Headteacher appointments, which are subject to greater scrutiny than other teachers, it says “…headteacher vacancy, advertise the post as appropriate (unless it considers it has good reason not to)”

In my opinion then there are a number of “good reasons”

The vetting process for the current member of staff has already been satisfied

The selection process was followed before their original appointment

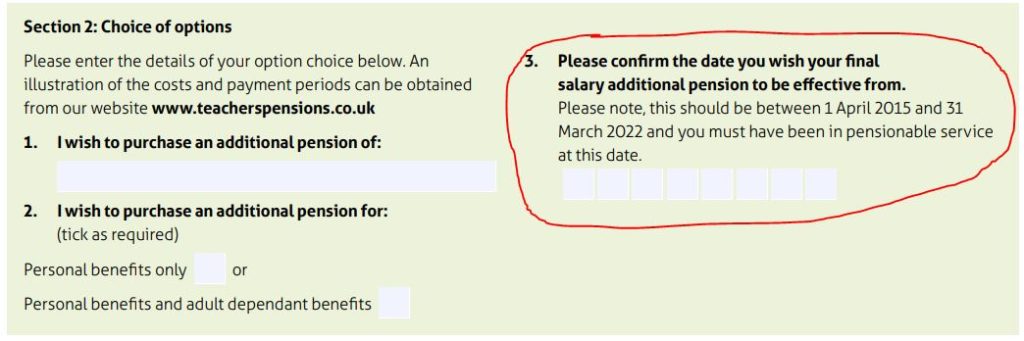

Up until this point we have been told to complete the old form and include a covering letter requesting the application be taken for additional pension (AP) to be purchased in the final salary scheme during the remedy period.

Before I start going into the details of this there are some parts which are not completely clear and so I must warn you that the figures may not give a true and accurate picture. However, the figures I do have are from an application made for retrospective AP. This date is asked for on the new application form in Section 2

I am going to assume that the “Pension Increase” will be applied from the date that the additional pension (AP), however this is not certain to be the case as the letter I have seen says this: “Your Additional Pension increases in value from the date of your full payment to your retirement date in line with pension increase factors.“

I am basing my assumption though on the fact that the payment requested does include an element of interest based on the time that has passed since the date asked for in Section 2 above. I don’t believe you can charge interest on something if you then take the date of the payment as the basis for applying the value of what has been bought.

Figures for 2016 – 50 Year Old

AP has to be bought in blocks of £250 but for the purposes of this post I will look at purchasing 4 such blocks, totalling £1,000. The date for this to be taken as 2016. I will also include the purchase of family benefits (50% to a partner etc)

£1,000 of FS AP (2016) would cost £16,080. Interest charged £1,382.

My Analysis

The interest for nearly 8 years is only 8.59%, that’s a simple annual interest rate of somewhere between 1.0% and 1.3%. That “feels” like good value.

Pension Increase: from 2016 to 2024 the inflation rate is in the region of 31.87%. If this is applied to the £1,000 then it would be worth £1,318.70 now.

Age to recover the investment

If the Pension Increase is applied from the elected date of purchase, which I believe it should, then dividing the cost (£17,462) by the current value (£1,318) gives us 13.3 years.

Taken at 60 that would be by 73.3.

If I am wrong about the way the PI is going to be added then it wold take 17.5 years to recover the investment, so by the age of 77.5

Compared to buying AP in the CA scheme now

The question here then, is it better to buy retrospective FS AP or to buy AP in the current career average (CA) scheme. For this comparison bear in mind that a 50 year-old in 2016 would now by 57/58.

A 57 year-old buying £1,000 of CA AP (2024) with family benefits would pay £15,160. That would take them 15.2 years to recover that investment. However, this AP would only be paid, in full, if they started taking it at 67.

67 plus 15.2 means they would get their investment back at the age of 82.2

I would suggest, therefore, that if you are considering the purchase of additional pension then it would be far better value to make an application for the retrospective purchase of AP from the remedy period than to buy it in the current career average scheme.

With the “rollback” taking effect every, eligible, teacher has had their 2015-2022 service returned to the final salary scheme and as a result “overtime” causes an issue for the administrators.

Overtime is NOT pensionable under the final salary scheme but IS pensionable under the career average scheme.

This means that if you had overtime in the remedy period you paid the pension scheme around 10% of that in return for some pension, just the same as you do for your normal wages. However, that should only happen if you are in the career average scheme and not if you are in the final salary scheme. The “solution” is for the scheme to refund you what you paid, but they really do not explain what you may be giving up if you take this refund.

This video goes into your real options and consequences.

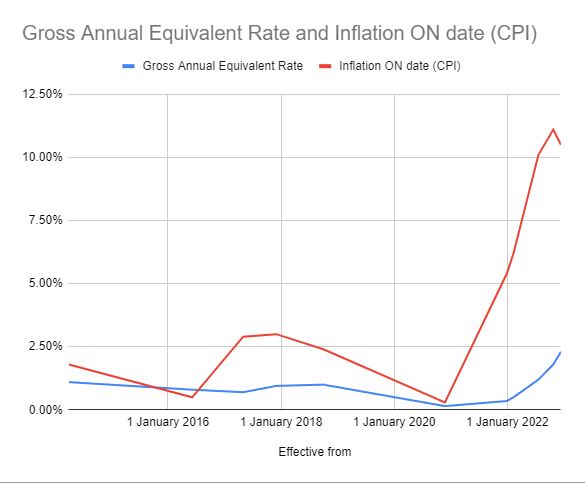

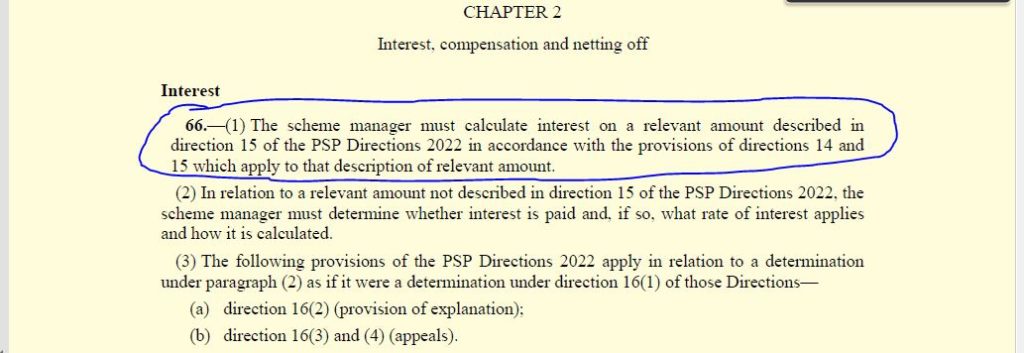

One of the details hidden away as a reference to another document and then a reference from that document is the amount of “interest” that will be added to amounts owed to members for underpaid lump sums and pension payments.

Interest 66.—(1) The scheme manager must calculate interest on a relevant amount described in direction 15 of the PSP Directions 2022 in accordance with the provisions of directions 14 and 15 which apply to that description of relevant amount.

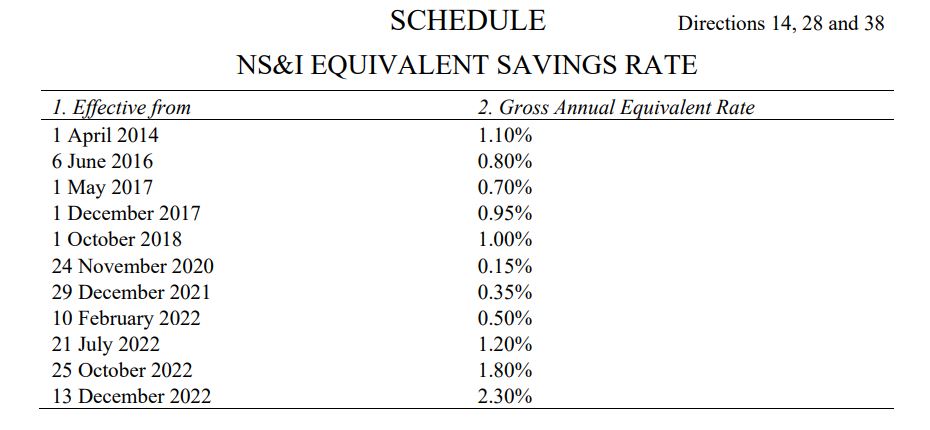

On page 40 of this document is the table that lays out what the “interest” amounts will be…and they fall a long way short of inflation!

For comparison I have added a column to this table showing the inflation factors that were in effect on the dates shown:

The Government has confirmed that the annual cost of living increase, based on inflation from the previous year, will be applied from this April at 10.1%

As well as increasing pensions that are already in payment this figure is used to uprate the historical salaries used in the calculation of the final salary figure.

The Teaching pension schemes are no strangers to changes in the pension age at which they are designed to be taken.

Before 2007 it was 60, then 65 and more recently has been brought into line with the state pension age. What is also changing is the MINIMUM pension age – the age at which you can, with a reduction, take the pension.

The GOOD news, for some, is that if you were paying into the TPS before the Government announced the change to the minimum pension age then you will retain the right to take the pension from 55.

Key date: 4 November 2021

If you were IN the scheme before 4 November 2021 then you do retain the right to take your teaching pensions from 55.

The BAD news for some then, is that if you started after this date then, from 6 April 2028 you will cannot take it before 57. (Unless via an ill-health retirement)

The Government’s plan is to raise this further in the future to 58 and for it to then track 10 years behind the state pension age. Remember though that taking it 10 years early does mean you will be paid less to make up for the fact you will be paid it for longer.

Transferring your private pension into the Teachers’ Pension Scheme when you start teaching may give you a better annual pension than buying an annuity…if you live long enough to enjoy it