The McCloud judgement declared that the transition of public sector pensions introduced in 2015 was illegal. This explains the relevance to the Teachers’ Pension schemes.

Reflections on reaching for retirement

The McCloud judgement declared that the transition of public sector pensions introduced in 2015 was illegal. This explains the relevance to the Teachers’ Pension schemes.

Pensions are a fraction of your salary. (80th, 60th, 57th etc) so does taking a pension mean having to watch every penny…it’s not as big a cut as you may think.

youTube: Poor Pensioners – Just how big a drop in income is it?

One of the biggest myths, or misunderstandings, is that taking the pension ‘early’, as early as 55, LOSES 20% of your pension.

There is some truth to this figure but it is NOT as significant as it first sounds…I explain more here

Shockingly bad adding up…

This is an appallingly bad presentation of figures sent to a teacher – I have “mentioned” this to the TPS and the teacher is making their own complaint…along with two others that have also contacted me with the same problem.

They have been given two “totals” but the totals come from two different time periods, 3 years apart.

The totals given to them make it look as though one of the options will pay £1800 more than the other, but when the pensions are valued to the same date the difference is only £1000. As there is also a significant gap in the lump sums someone could easily have made a different choice based on the figures as presented.

At no point in time would the pension total given in this example for Option 2 ever had been paid…it is just complete and utter nonsense!

Here is what looks like a MAJOR systemic problem with RSS’s being provided to teachers who took their final salary pension WITHOUT taking their career average one and who are now applying for the career average. Please do pass on my concerns about this, I have now seen 3 of these and have asked the members to make their own complaints to you. However, given that this no longer appears to be an isolated case I am posting this here.

The problem:

1) The final salary pension is given the value it would have had at the time it was taken, in the example here (posted with the permission of the owner), that is to 1 March 2022.

2) The career average pension is given a value to a different date. In this example to 18 May 2025.

3) These two values are then added together to give the “Total Annual Pension” which is a nonsense.

The final salary row is valued to 2022 and the career average to 2025. To get a comparable total they must BOTH be valued to the SAME DATE.

For reference I have overlaid the image of their RSS with those calculations using the PI factors published for such by the Government.

The consequences:

The RSS as provided suggests that there is a difference of £1,833.60 in the annual pensions between options 1 and 2. The reality is that the difference is £1,051.42.

A reduction in the difference of well over 40%.

The production of these figures for those in the situation I describe MUST be halted immediately and anyone who has been sent such figures and made their choices based on such misleading numbers must be contacted, provided with comparable figures set in the same time frame and be permitted to change their choice if it has already been made.

Help – my employer is insisting I need a break in employment!

January 2025

I received this plea from a teacher who was in the process of getting agreement to take “phased” retirement.

The employer was, mistakenly, insisting that there had to be a break of at least one day between contracts – something that is most certainly NOT a requirement for PHASED retirement….EARLY retirement is another matter of course.

The response I coined for them was this:

I can see that there is some confusion over the need, or not, to have a day’s break between contracts.

Previously there was no such thing as “phased” retirement and I believe the policy you are referring to relates solely to what is known as “early” retirement.

The need to have a break between employments to take “early” retirement is clearly noted in the most recent set of regulations, “The Teachers’ Pension Scheme Regulations 2014”, where, in regulation 104(c) it states that to be entitled to an early retirement pension the person, and I quote, “has left all eligible employment” on the day the pension starts.

However, the whole point of introducing “phased” retirement was to allow teachers to continue without requiring a break in employment. Indeed, such a break, if it were to take place after the teacher had reached the “normal” pension age, would prevent the teacher from taking a “phased” retirement as it triggers the “normal age” retirement.

In Chapter 3, which regulates the new “phased” retirement option, it is clear that there is no similar requirement for there to be a gap in employment or for a whole new contract.

Indeed regulation 90 makes it clear that a person can be continuing in employment so long as the terms change and that they are not earning more than 80% of their previous rate.

To quote regulation 90:

“90. A person (P) meets the reduced annual rate condition if—

(a) P is in one or more eligible employments;

(b) the terms of employment change and as a result there is a reduction in the annual rate of P’s pensionable earnings; and

(c) the reduced annual rate is not more than 80% of the average annual rate of P’s pensionable earnings for the 6 months of pensionable service immediately before the reduction.”

Taken together this clearly indicates that this is not a new contract but simply a change in the terms of the contract.

To make it even clearer that a new employment under a new contract is not required we can look further to regulation 93 that determines a teacher’s entitlement to a phased retirement pension:

To quote

“Entitlement to phased retirement pension

93.—

(1) A person (P) is entitled to payment of a phased retirement earned pension from the entitlement day if—

(a) P has reached normal minimum pension age but has not reached 75;

(b) P is qualified or re-qualified for retirement benefits;

(c) P meets the reduced annual rate condition or the new employment condition;

(d) P has made a phased retirement application; and

(e) P has not applied under regulation 162 for payment of any other retirement pension.

(2) P is entitled to payment of a phased retirement additional pension from the entitlement day if P has applied under regulation 94 to receive an additional pension with the phased retirement earned pension.

(3) Subject to regulation 97, a phased retirement pension is payable for life”

93(c) is clearly the part that is leading to the confusion we are having to deal with.

The word “or” being the key element.

Where the TPS have said, and I quote “If a staff member is submitting a phased Retirement form, they can leave and return 1 day later on a reduced contract.” they have given only half an answer. Yes, the staff member CAN leave and return on a reduced contract but that, under 93(1)(c), is only the latter part of what they CAN do. They CAN also become entitled to a phased pension by meeting the reduced annual rate condition. One does not preclude or require the other.

Half an answer from one member of the TPS help desk should not be taken to mean any more than it says and when you look at their factsheet, published in April 2024, this document is crystal clear in its assertion that, unlike the other types of retirement – such as the early retirement that I have quoted previously and that I believe you are working under the misconception that those conditions also apply to phased retirement, phased retirement most certainly does not require a break in employment.

https://www.teacherspensions.co.uk/-/media/documents/member/factsheets/applying-for-retirement/phased-retirement-factsheet.ashx

To quote “You don’t have to take a one day break in employment to take Phased Retirement (as you do with other types of retirement in the Scheme).“

Your employer is allowed to deny permission for you to take “early” retirement for up to 6 months….is that for real?

There is a rule that says that if you are applying for “early” retirement then your employer has to “agree”.

A first sight the rule appears to be rather punitive, but once you drill down into the detail there is a “get out” clause and it is only when you understand why the rule was conceived in the first place does it even make any sense at all.

Your employer is entitled to withhold their permission for up to 6 months.

However, the “get out” clause is exactly as it sounds. Their denial of permission only lasts for as long as you are employed by them.

Their blocking of your application ends on the very last day of your employment, though you must have given the TPS at least 6 weeks notice.

Regulation 12(3)(b) under Schedule 7 (Case E: early retirement):

(b) where P ceases to be in that employment before 6 months have expired since the date on which P asks P’s employer to agree, such day as P specifies in the application, which must be no earlier than 6 weeks after the date on which P’s application is made.

https://www.legislation.gov.uk/uksi/2010/990/made/data.pdf

The rationale for this rule’s inclusion is that the pension scheme is not allowing a teacher to get around their contract of employment and take their pension whilst still “employed”.

A teacher has to give a minimum of 3 months notice to leave their employment and this rule is designed to prevent a teacher walking out of their contract and taking the pension immediately.

So, yes, taking the pension “early” requires you get the permission from your employer, but so long as you ASK for it, and apply for the pension, at least 6 weeks before the end of your employment contract it doesn’t matter if they give or deny you that permission since your pension will be paid on the first day after leaving employment so long as you have given the required notice to resign your employment.

Just my collection of thoughts on ways the statement and other aspects of the TPS could possibly be improved.

Where a Method B calculation for the final “average salary” is using salaries that are about to become too old then the statement could include something to alert the teacher to this fact. Possibly colour-coding the months/years that are being lost, I would suggest red for those being lost in the next 6 months and amber for those that will be lost within 12 months.

To be included on the statement, though this may be an issue of cost since every break creates a new calculation and some teachers, particularly supply staff, could have rather a lot of these.

Alternatively, including the final “average salary” that was in effect at the time of each break since this is a value critical in determining if the break is going to give rise to a “restricted” or “unrestricted” hypothetical calculation.

Currently the indexation figure being used for the year does not get added to the estimated pensions on the statements until the Government confirms it will use September’s CPI measure of inflation. The Government doesn’t tend to do this until the first months of the following year despite the figure being published by the ONS in October.

Given that the statements are only considered to be “estimates” there is no reason that once the inflation figure is published it could not be factored in to the calculation.

Publishing, and then updating regularly, how many RSS’s need to be produced and the number currently distributed would give members a better understanding of the scale of the problem and appreciate how quickly it is being resolved, or not.

I would expect there to be a process that is followed rigorously when an application for a pension is made. The current task tracker lacks details on what those steps are and whether there are any sticking points.

A list of the steps with green ticks for complete, amber for steps that are waiting for 3rd party action and red for those that cannot be completed until prior steps are completed would give more reassurance that the application was being processed.

The conversion letters sent out to those who purchased extra pension in the remedy period offer compensation or a conversion to additional pension in the final salary scheme but the figures are not comparable.

The compensation is based on the value now, currently in 2024, but the conversion figures are either based on a value from April 2022, if the extra pension purchased is via Faster Accrual or the Early Buy Out, or the value from the date the original purchase of additional pension was made, potentially as far back as April 2015. The newest letters do tell teachers than indexation has to be applied from those dates but it would make far more sense to give them the valuation as of April 2024 as well.

In the years leading up to a teachers normal pension age, 60 for those in the scheme prior to 2007 and 65 for those who joined between 2007 and 2015, that taking the pension on, or after, reaching the pension age invokes the rules on abatement if they continue in TPS-eligible employment

The structure of the message service on the website is geared to a single message and single response model. Great if the person responding answers the question being asked completely but confusing if follow up questions are required or they miss the point of the question.

Allowing messages to be threaded would remove the need to constantly repeat a whole message and clarify why the response sent was inadequate or misdirected.

The option to set a “subject” for the message would allow the sender to be able to find a specific message, at the moment they almost all have the same generic subject and reference:

Where part time teachers have concurrent contracts the part time earnings column can often contain just a 1.00. This makes it nigh on impossible for teachers to work out if the payment, and therefore the pension entitlement, matches what they have been paid for during that period.

Held up for many months (even years) due to waiting for “something” it shouldn’t be necessary for a manual calculation of this to be asked for.

Members report that they cannot simply use the password “reset” function at times and when they finally get through to a support agent it is because the account has been “locked” and requires the agent themselves to reset it. A message to this effect would reduce frustration and speed up the reset process. (Having a “code” to quote to the agent could lead the agent directly to whatever support document is required to action the process)

Teachers are reporting that during the application process the “data cleanse” operation undertaken by the TPS administrators often throws up anomalies in the service history, often going back decades.

In my opinion many of these problems could have been identified earlier and questioned at the time when records are still intact. With the advent of GDPR many employers no longer keep records going back more than 7 years, identifying and correcting errors at the time is much more likely to lead to the correct data being used.

Classic errors that we see time and time again for which an automated process to identify them sooner should be possible include:

In 2007 the concept of the “disqualifying break” was introduced that had two significant impacts on the pension previously built up in the TPS

A disqualifying break is one that exceeds more than 5 years, BUT if the member was employed in another public sector post and paid into their pension scheme during that period then that can be used to “reset the clock” that measures the 5 year break. (Regulations 65 and 66 of the The Teachers’ Pension Scheme Regulations 2014)

Yet there is NO MECHANISM for proactively checking if the member, upon their return to the TPS, has had such service and as such there will be a number who are probably being underpaid when they take their pensions.

In a response to a FOI request to the DFE I was told “The onus is on the member to provide us with the information about their membership of other public service pensions schemes…”

In my opinion the scheme should be proactively ASKING a member when they return after a break of more than 5 years if they have any qualifying service in other pension schemes to ensure that they are put into the correct scheme and with the appropriate conditions. Simple assuming that they have no service in other relevant schemes is an abdication of responsibility.

Those applying for ill health retirement are some of the most vulnerable members of the scheme, often at the lowest points in their lives and we have had reported that some have been receiving letters that are incorrectly advising their applications have been refused, whilst also containing the medical reports from the TPS’s own team stating that they should be approved. Upon challenging these letters it has been reported that the covering letter had been incorrectly selected and used.

With those receiving these letters already at their lowest points it doesn’t take much thought to realise that these could have lethal consequences.

The procedures for sending this letters MUST be changed to ensure that such an error cannot happen.

Schools/employers can change the records at any time and going back as far as they like. This is necessary where the records are incorrect of course, but there is NO warning given to the teacher by either the employer or the administrators of the TPS when this happens.

Any “update” to the record by an employer may be WRONG.

The administrators of the TPS should alert the teacher when a change is made to the historical records so that the teacher has the opportunity, at the time, to verify that the change was appropriate and, if necessary, to challenge the change with their employer.

With employers no longer being required to retain employment records for more than 7 years any mistakes made in such updates can become very difficult to correct if they are not identified in a timely manner.

For example, a school “updates” the wrong teacher’s record for an employment held 20 years ago having been given the evidence by a different teacher despite having no evidence of their own for this. The person at the school who made the update then might leave that employment and the incorrect update doesn’t come to light for another 20 years. There are then no records held by the school and nobody who can remember that an update was made. It becomes impossible for the school, or the wronged teacher, to put 2 and 2 together to work out what has happened.

If the TPS informed the teacher at the time the update was received from the school the teacher would have the chance to challenge it whilst the person who has made the change to the records would still be available to respond.

This is an appalling and, likely, a systemic problem.

I have been sent a number of statements where the two options have had the headline total “created” by adding the final salary and career average component parts where those parts have been valued to different periods in time. An FS pension valued in 2022 would be 17.48% LOWER than in 2024. This image shown shows the problem as the option 1 total would be, in 2024, worth £25,123 and option 2 would be £25,006…REVERSING which is the BEST annual value!

A second and even more dramatic example is shown in this: https://dfountain.co.uk/22-does-not-equal-4/

This is a common topic I get asked about, normally from the angle of someone who is looking to get a bit more money NOW…understandably of course. This is a post I made on the Facebook group in response to one such question.

I do always feel a bit like Marie Antoinette telling others to “Let them eat cake” when I talk about this aspect of the scheme – and note a trigger warning, I will be talking about death and distressing circumstances shortly.

The pension is better value for money whilst on maternity leave.

You pay the same % of your wage throughout, but as maternity pay drops this means you pay less. (I will assume 10% = £400)

For this however, the amount your pension gets credited with (1/57th) remains the same all the time you are on at least statutory maternity pay. (£70)

(With tax you would only get 80% of the amounts you pay into the pension).

My apologies but I am going to be blunt.

Take a worst case scenario. You die and your child (or children if twins etc) survive.

Having opted out they would miss out on:

1) the much greater death-in-service grant

(Three times what would be your full time salary instead of, roughly, three times your pension), and

2) the enhanced survivor’s pension for the next 18-23 years of their life (lives).

(The enhancement adds half of what you would have added to your pension between now and your state pension age).

Your partner would also miss out on getting an enhanced survivor’s pension as well.

Whilst I would urge you not to leave the pension scheme I appreciate that I do so from a position of privilege, if you are in a position where this makes the difference you decide is critical then it is one you can make, I hope that what I have said though allows you to do it with a greater understanding of what the cost to your pension might be.

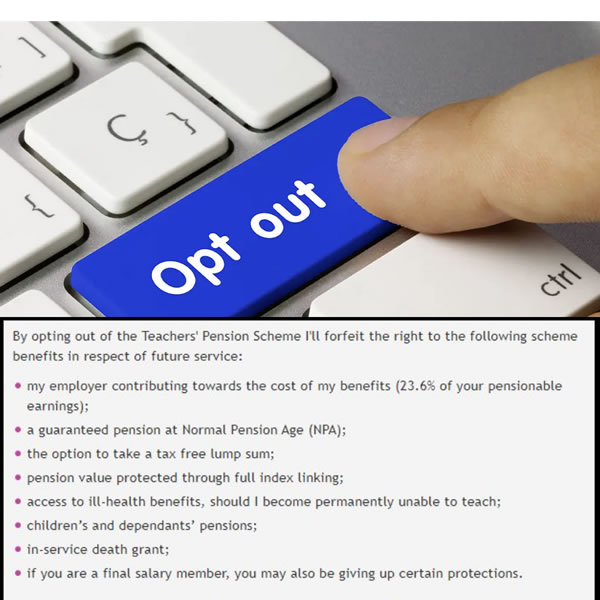

The WARNING!

When you go to opt out you get “warned” about doing this with a list of what they consider the dire consequences…bear in mind that this list is aimed at those who are thinking about opting out of the pension scheme for good and not those who are looking to “lock in” a good set of salaries that could soon become too old to be used and may be lost forever without such action. Opting out to invoke the protective hypothetical calculation is not the same as leaving altogether.

However, the warnings do worry people – that is the intention, after all, to make those thinking about leaving, pause for thought. There are some parts that are relevant but here I go through each of the points being made.

| my employer contributing towards the cost of my benefits (23.6% of your pensionable earnings); | 1) Employer contributing 23.6%. It doesn’t matter how much they contribute. The calculation of your final salary is based on rules and not on how much money is paid into the scheme. Opting out to use the hypothetical calculation “rule”, to stop the value falling is the point of doing this. It is one of the most counter-intuitive rules that means you can get MORE by paying in LESS (one month less). But it is a rule and there to be used if you are aware of it. (oh and it is rising to 28.6% in April 2024 – but it still doesn’t matter) |

| a guaranteed pension at Normal Pension Age (NPA); | 2) Guaranteed Pension at NPA You do not forfeit your right to what you have already bought and paid for in the scheme. Indeed what you are doing is locking in what you hope is likely to give you a BETTER guaranteed pension, at the same NPA. (Opting out for a single month means you come back into the same scheme you would have been on if you hadn’t opted out. Only a break of more than 5 years can change that, AND only if they changed the scheme during that break) |

| the option to take a tax free lump sum; | 3) Tax-free Lump Sum entitlement Unless they change the rules of the scheme this doesn’t happen. Again you would have to be out for more than 5 years and the change happen whilst you were out. |

| pension value protected through full index linking; | 4) Pension value protected through index linking. Yes, this is the whole point of opting out, to lock in what have turned out, already, to be HIGHER valued salaries from the past before they get to old to be used. Indeed, opting out, for just one month, is protecting the pension’s value – it is staying in, without a break, that could lead to a loss of value if your best salaries get too old to be used in the calculation of the pension. |

| access to ill-health benefits, should I become permanently unable to teach; | 5) Access to ill-health benefits. YES, this one has some merit and is the reason why many suggest taking out extra insurance for the month you are out of the scheme. However, note that you do not “lose” those benefits permanently, they are restored, in full, upon re-joining the scheme. Note also that for your to become so suddenly ill during a single month out that you were fully incapacitated would be highly unusual. You get 6 months full sick pay and 6 months half sick pay, so unless you are already exhausting your sick pay entitlement it would be highly unusual for you to suffer a loss in this regard during a single month out. |

| children’s and dependants’ pensions; | 6) Dependent’s Pensions YES, again, this one has some merit and the point about insurance above applies. Dependent pensions, those given when you die, are much better if you are “in” the scheme at the time you die. The pension is enhanced by adding on half of what you would have added to the pension between the date of your death and your state pension age. Then a partner would get 37.5% of that and dependent children up to half what the partner would get. |

| in-service death grant; | 6) Death Grant YES, same as above, if leaving money to your heirs is important then consider taking out extra insurance. |

| if you are a final salary member, you may also be giving up certain protections. | 7) Final Salary Benefits This ONLY applies if you are out of the scheme for more than 5 years. The benefit referred to here is being able to use future salaries in the calculation of the final salary pension. Being out for a single month has NO impact. Also, given that you are opting out because the salaries from 8 to 10 years are are better than your current salary it would take some significant pay rises in the future for your future salaries to catch up and then overtake the ones you are locking in anyway! |

https://www.legislation.gov.uk/uksi/2010/990/made/data.pdf

The Pension scheme lays down very clearly how long a break is needed in order to take the pension before you reach you Normal Pension Age:

The Schedule in the regulations that covers taking “Early” retirement starts on page 121 and is called “Case E”

Case E: early retirement with actuarial adjustment

Page 121, Case E (10), https://www.legislation.gov.uk/uksi/2010/990/made/data.pdf (The Teachers’ Pensions Regulations 2010)

10.—(1) A person (P) falls within this paragraph if—

(a) P was in pensionable or excluded employment at any time after 29th March 2000,

(b) P ceases to be in such employment,

There are other parts to this regulation but the key part above is that you have to “cease” to be in employment. This is then expanded on to explain what is meant be “ceasing” in regulation 14, shown below:

For the purpose of this Schedule—

Page 122, Case E (14), https://www.legislation.gov.uk/uksi/2010/990/made/data.pdf (The Teachers’ Pensions Regulations 2010)

14 (a) a person is not to be treated as ceasing to be in pensionable or excluded employment unless at least one day passes without the person being in such employment after the person ceases to be in such employment;

Simply put, you can take the pension early so long as you are not employed as a teacher ON the day you have asked for the pension to begin.

Unfortunately many schools and LAs get confused over what is a break in employment, using what is needed to reset other employment rights and not what is needed for an employee to take their pension. There is no legal barrier to an employer ending, with the agreement of the employee, a contract of employment on one day and starting a new contract after a gap of 24 hours.

A number of schools HR departments are rather lazy in this regard and instead of just doing what is required to enable the employee to take their pension insist on a longer break because of their misunderstanding of what is needed to constitute a “break” in employment. This is often based on other employment rights, such as avoiding having to repay redundancy payments, or entitlement to sick pay etc.

Unfortunately, if they do insist on a longer break there is very little the teacher can do in such circumstances since they are over a barrel as they do need the break in employment in order to start taking the pension before their normal pension age.

This is NOT the case for teachers who have already reached their scheme’s normal pension age. They can start payment of their final salary pensions simply by opting out of the pension scheme without needing any break in employment.

This is the key question to ask HR advisors who are insisting that a longer break is required. The answer, of course, is “no”.

Another key question, to which the answer is also “no”

There are guidance and Statutory Instruments (SI) on how staffing in schools should be undertaken, and both of these documents have NO requirement that a break in contracts be of any given minimum length, nor that a post has to be advertised and the member of staff made to reapply for their position.

Even for Headteacher appointments, which are subject to greater scrutiny than other teachers, it says “…headteacher vacancy, advertise the post as appropriate (unless it considers it has good reason not to)”

In my opinion then there are a number of “good reasons”

“

How it works.

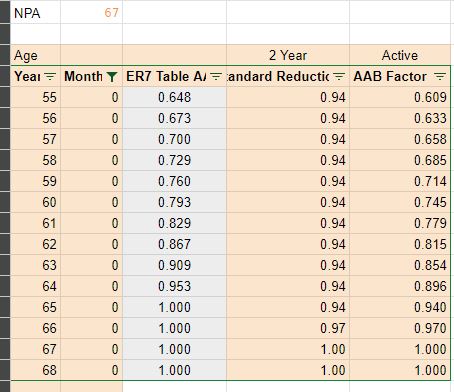

The question was, how long do you have to pay when you sign up for the Early Buy Out option.

Forever, or as long as you want, is the answer

Let me explain how it works.

Every month you add a bit to your pension (1/57 of that month’s salary).That bit will pay out when you claim your pension, being paid every year for the rest of your life, but will be reduced if you take it early.

The reduction is based on your age.This reduction is done in two parts because it is based on the State Pension Age (SPA) and people have different SPAs.

The earliest SPA is 65. If your SPA is later then 3% more reduction is applied for each year later your SPA is than 65. It is this latter 3% reduction that you can “buy out”. You can only buy out the number of years between 65 and your SPA.

If you take the pension at 55 then the reduction factor from 65 is 0.648.If your SPA is 67 then a further 0.94 factor is applied (2 lots of 3%).

Example. An unreduced pension of 10,000.

In just the same way that you add a bit every time you are paid to the pension if you elect to buy out you pay a bit more for the advantage of the buy out. Every month.

What happens is that the “bit” you add to your pension in that month will get the advantage if, at the same time, you paid extra for the buy out.

If you stop paying for the buy out then whatever you add to the pension in the next month won’t get the benefit. However, all the amounts you did pay for earlier will still get it.

Example. You pay for the buy out on the first £5,000 that is added to your CA pension. You then go on to add another £5,000 without paying for the buy out.

So you have £5k with and £5k without.

The calculations then for taking it at 55 are a mix of the two I put earlier, thus:

Total Pension: £6285.60

This image shows the factors and combined factor for different ages based on someone with an SPA of 67 buying out 2 years.

So you found a dodgy break in your history?

Over 90% of problems with the pension can be traced back to incorrect records being sent in to the administrators by employers.

The responsibility for putting errors right lies with the employer, the administrators (TPS) of the scheme have very limited powers to alter the records they have been sent, mainly only in cases where the employer no longer exists.

Contact your employer and explain the problem and ask them to correct it.

They may be willing to do that immediately but with many employers no longer keeping records for more than 7 years you may find that they want YOU to prove that they employed you and that you were in the pension scheme.

PAYSLIPS: The very best evidence is your pay slips that show that the school employed you AND that you were paying into the pension scheme. The problems if often that we no longer have our pay slips and it can be many years, decades even, in the past that the problem exists.

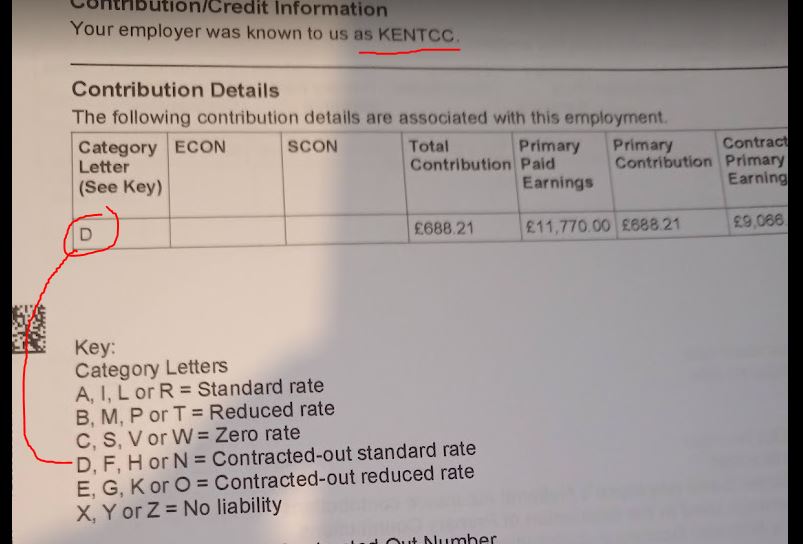

NATIONAL INSURANCE RECORDS (Pre-2016): HMRC keep records going back to the day you were issued with a number! As such you can ask them for this data and it is, for employment before 2016, very useful proof.

Before 2016 teachers who were paying into the TPS paid a special rate of National Insurance and so this is recorded by HMRC. It is called the “contracted out” rate. Ask TPS for your records of employment and the NI rate and it will show you, for periods up to 2016, both who employed you and whether you were in the TPS or not.

Look for the employer and the “Category Letter” for the employment as proof you were in the TPS

Make a “Subject Access Request”: https://www.gov.uk/guidance/hmrc-subject-access-request

Ask HMRC for the following:

If you are in a Union see if they can get you legal help to draft a proper letter advising the employers of their legal responsibilities and potential liabilities if they fail to address this issue in a timely fashion. If you are not in a Union then check to see if you have legal protection included on your home insurance.

You also have the option to refer the matter to the Pensions Ombudsman for “maladministration”.

The kind of thing that we have heard can get results is to “remind” the employer of the potential costs to them if they do not get it sorted, nagging them repeatedly and making it “easier” for them to resolve the situation – keep squeaking.

Run this by a lawyer but something along the lines of…”The records of my employment history for the purposes of calculating my pension as held by the Teachers Pension Scheme administrators (TPS) for my time in your employment from dd/mm/yyyy to dd/mm/yyyy are wrong. I am informed by the TPS that only you as the employer may make corrective updates via the monthly data collection that they require you submit to them. I have also been advised that should <name of employer> fail to make the necessary corrections in a timely manner and that as a result I were to suffer any unavoidable financial losses then <name of employer> may become liable to cover such losses. The Pensions Ombudsman may in addition, upon finding a case of maladministration, direct the employer to make financial compensation for distress and inconvenience. The scale of such compensation rising when the employer has not demonstrated that they have taken action to address the complaint. As I have not heard from you since I last communicated on this matter since dd/mm/yyyy then I must start to consider taking such actions.

My preference is, of course, to have the records held by the TPS in respect of my employment with <name of employer> updated to correctly reflect my service with <name of employer>. Specifically ((((now insert what you want the data to show)))).To avoid increasing the anxiety this matter is causing me and to alleviate the distress please can you communicate to me within 15 working days what steps you have taken to provide the TPS with the necessary corrective update to the employment records held by them on your behalf.”

In response to my complaint that no method for applying for retrospective was available I have received the following response.

There were 3 points I made that I felt needed to be addressed

The first of these has now been addressed, with a form for applying for retrospective additional pension now available: https://www.teacherspensions.co.uk/-/media/documents/member/applications/miscellaneous/apb-december-2023-v18-fs.ashx

The second and third have been ignored, though the response I have received does give the costs for two ages.

Proudly powered by WordPress | Theme: Baskerville 2 by Anders Noren.