Up until this point we have been told to complete the old form and include a covering letter requesting the application be taken for additional pension (AP) to be purchased in the final salary scheme during the remedy period.

Before I start going into the details of this there are some parts which are not completely clear and so I must warn you that the figures may not give a true and accurate picture. However, the figures I do have are from an application made for retrospective AP. This date is asked for on the new application form in Section 2

I am going to assume that the “Pension Increase” will be applied from the date that the additional pension (AP), however this is not certain to be the case as the letter I have seen says this: “Your Additional Pension increases in value from the date of your full payment to your retirement date in line with pension increase factors.“

I am basing my assumption though on the fact that the payment requested does include an element of interest based on the time that has passed since the date asked for in Section 2 above. I don’t believe you can charge interest on something if you then take the date of the payment as the basis for applying the value of what has been bought.

Figures for 2016 – 50 Year Old

AP has to be bought in blocks of £250 but for the purposes of this post I will look at purchasing 4 such blocks, totalling £1,000. The date for this to be taken as 2016. I will also include the purchase of family benefits (50% to a partner etc)

£1,000 of FS AP (2016) would cost £16,080. Interest charged £1,382.

My Analysis

The interest for nearly 8 years is only 8.59%, that’s a simple annual interest rate of somewhere between 1.0% and 1.3%. That “feels” like good value.

Pension Increase: from 2016 to 2024 the inflation rate is in the region of 31.87%. If this is applied to the £1,000 then it would be worth £1,318.70 now.

Age to recover the investment

If the Pension Increase is applied from the elected date of purchase, which I believe it should, then dividing the cost (£17,462) by the current value (£1,318) gives us 13.3 years.

Taken at 60 that would be by 73.3.

If I am wrong about the way the PI is going to be added then it wold take 17.5 years to recover the investment, so by the age of 77.5

Compared to buying AP in the CA scheme now

The question here then, is it better to buy retrospective FS AP or to buy AP in the current career average (CA) scheme. For this comparison bear in mind that a 50 year-old in 2016 would now by 57/58.

A 57 year-old buying £1,000 of CA AP (2024) with family benefits would pay £15,160. That would take them 15.2 years to recover that investment. However, this AP would only be paid, in full, if they started taking it at 67.

67 plus 15.2 means they would get their investment back at the age of 82.2

I would suggest, therefore, that if you are considering the purchase of additional pension then it would be far better value to make an application for the retrospective purchase of AP from the remedy period than to buy it in the current career average scheme.

After hearing again, for the umpteenth time, that you MUST have a break in employment to take the final salary pension I decided to put the answer here.

UNDER 60 (Final Salary scheme started before 2007)

Yes, to take this pension “early” you MUST have a break in employment.

60 or OVER

For the NPA60 scheme you do NOT need a break in employment, what you need is a break in “pensionable employment” and these are not the same thing. You can create such a break without leaving employment simply by opting out of the pension. You can, of course, create a break by leaving employment but you don’t have to.

2.—(1) Where a person (P) satisfies the condition for retirement, the entitlement day for Case A is— (a) if P is not in pensionable employment on the day on which P reaches the normal pension age in relation to the reckonable service, the day on which P reaches that age, and (b) if P is in pensionable employment on the day on which P reaches the normal pension age in relation to the reckonable service, the day after P ceases to be in pensionable employment.

Part 2 – Pensionable employment

Regulation 7 paragraph 3

(3) A person who makes an election under regulation 9 (election for employment not to be pensionable) is not in pensionable employment while the election has effect.

Images of the Application Form

These images taken from the application form, for “normal age” retirement also make it clear that it is sufficient to opt out, without leaving your employment, if you will reach the normal pension age and wish to take the pension.

With the “rollback” taking effect every, eligible, teacher has had their 2015-2022 service returned to the final salary scheme and as a result “overtime” causes an issue for the administrators.

Overtime is NOT pensionable under the final salary scheme but IS pensionable under the career average scheme.

This means that if you had overtime in the remedy period you paid the pension scheme around 10% of that in return for some pension, just the same as you do for your normal wages. However, that should only happen if you are in the career average scheme and not if you are in the final salary scheme. The “solution” is for the scheme to refund you what you paid, but they really do not explain what you may be giving up if you take this refund.

This video goes into your real options and consequences.

The Government has concluded the consultation and their response can be found here: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1173440/Teachers_Pension_Scheme_transitional_protection_regulations_consultation_response_.pdf

Points I have picked up on so far:

51. For tapered members (born between April 1962 and September 1965) there is a small chance that both options will be worse than what they currently get. Whilst there is no option for them to retain their better, current, position because it was at the root of the illegal age discrimination case, the Government have indicated that no repayment of the amounts already paid should be required.

56. Hypothetical calculations should, from October, be in included in the benefit statement – re-titled to be an RSS (Remediable Service Statement). This has been one of my particular irritations with the current statement so I am glad to see it is being addressed as not having the correct figures on the statement doesn’t help members make informed choices.

60.

70. Opting in and out for different periods is to be permitted but there appears to be a greater emphasis placed on the member being able to demonstrate why they would have made these choice compared to those who wish to re-instate the whole period.

71. Applying for service re-instatement is going to be subject to a 12-month clock starting on 1 October 2023. This I still believe to be contrary to the primary legislation as I detailed in my response to the consultation. If you did opt out of the pension scheme because of the changes then you will need to submit your application before 1 October 2024 but it does then appear that they will give you a further 12 months to confirm your choice.

80. Retrospective option to buy additional pension in the final salary scheme.

83. Early Buy Out window re-opened. Normally you have to make this choice in the first 6 months of joining the scheme but this will be opened again, for affected members, from 1 October 2023.

134. Lump sum (the optional additional lump sum). On taking the pension members were able to “sell” some of their annual pension for an extra lump sum. If they decide to put 2015-2022 back into the final salary scheme they will be able to re-visit that choice. My personal opinion is that selling part of the pension to get the larger lump sum is poor value for money and this option gives those who made that choice the opportunity to reconsider. Given that many will have been in receipt of the pension for a number of years they may now see the value of the index-linked part of the pension they gave up in a clearer fashion.

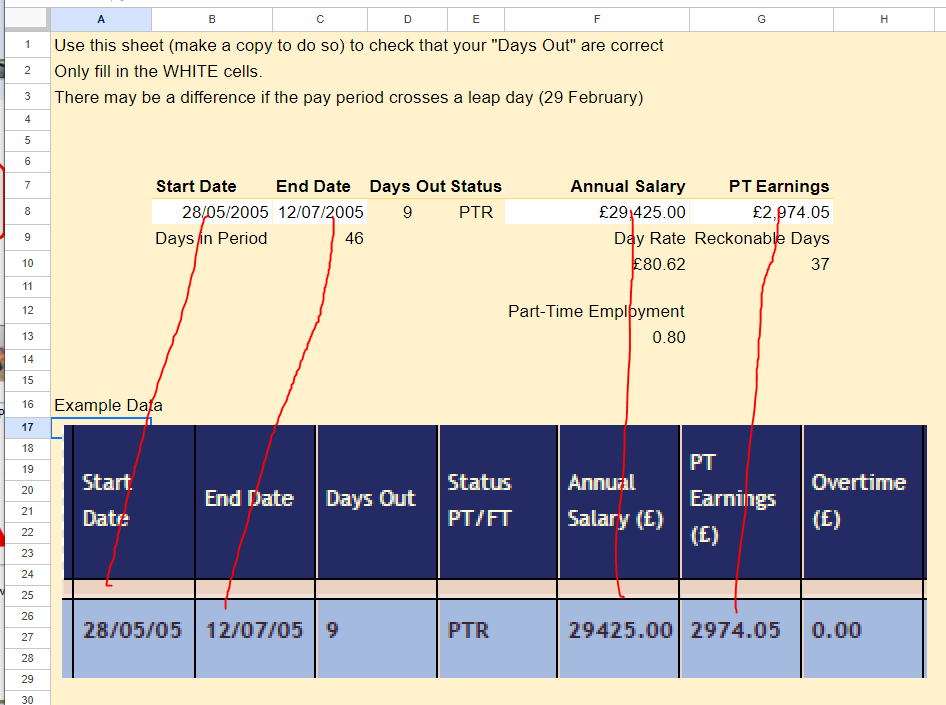

After fielding a number of queries regarding the days out and how they are recorded for part-time teachers I created this sheet to allow teachers to check their figures:

The way that part time work is recorded is not very intuitive and I sympathise with them. After all if you work 4 days a week then in a month you are likely to miss working on 4, or at the most 5, days in that month…so how come the statement shows 6 “days out”…there aren’t that many “Mondays” in ANY month!

To understand how part time service is recorded requires a different approach than just looking at the actual days you work in a week, we need to go much wider than that.

A full time teacher may work 5 days a week and they do that for 39 weeks in a year, that is 195 days, but their service record for a full academic year is recorded as all 365 days in the year (even in a leap year!)

In order for a part time worker to be credited with the correct proportion of the pension, i.e. 80% for one who works 4 days a week, that proportion is applied to each pay period. In a full academic year then a 0.8 part time teacher should get 0.8 x 365 days credited to their service record.

0.8 x 365 = 292 days. This is recorded by having the rest of the year, 73 days, labelled as “days out”.

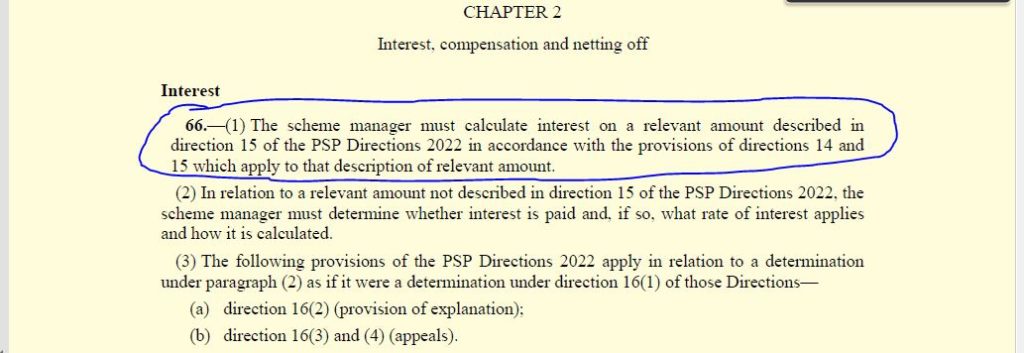

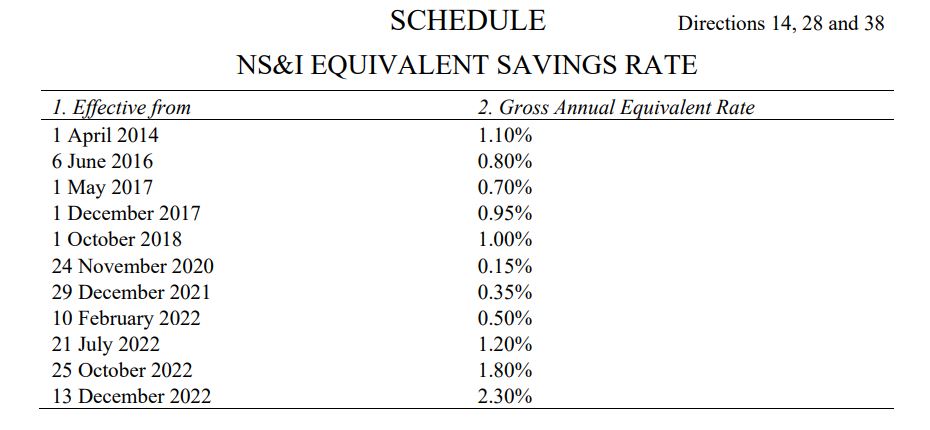

One of the details hidden away as a reference to another document and then a reference from that document is the amount of “interest” that will be added to amounts owed to members for underpaid lump sums and pension payments.

Interest 66.—(1) The scheme manager must calculate interest on a relevant amount described in direction 15 of the PSP Directions 2022 in accordance with the provisions of directions 14 and 15 which apply to that description of relevant amount.

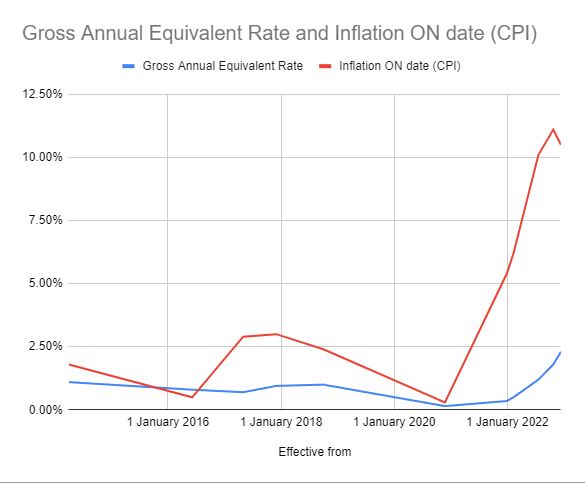

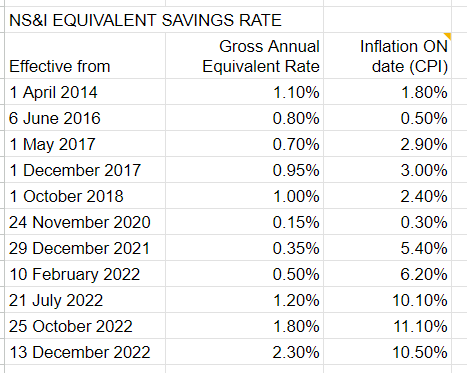

On page 40 of this document is the table that lays out what the “interest” amounts will be…and they fall a long way short of inflation!

For comparison I have added a column to this table showing the inflation factors that were in effect on the dates shown:

The Government has confirmed that the annual cost of living increase, based on inflation from the previous year, will be applied from this April at 10.1%

As well as increasing pensions that are already in payment this figure is used to uprate the historical salaries used in the calculation of the final salary figure.