Saving into a pension scheme can be a good way to avoid paying the higher income tax rates…but the question is how much are you likely to pay the higher rates on?

This sheet can help you assess how much you might be paying more than 20% on.

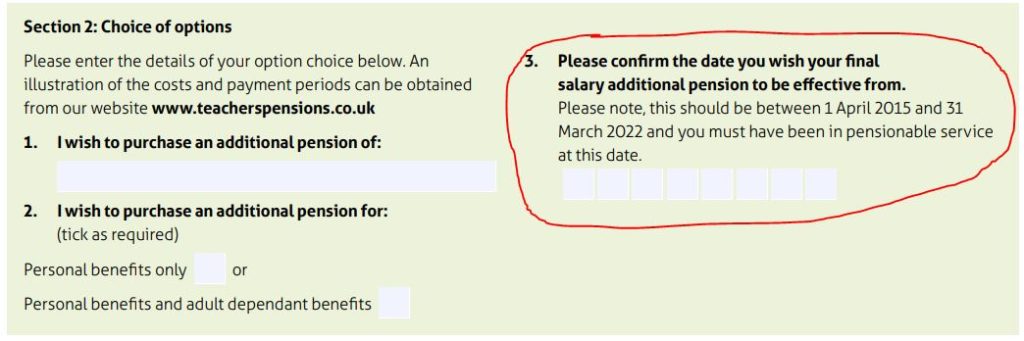

Up until this point we have been told to complete the old form and include a covering letter requesting the application be taken for additional pension (AP) to be purchased in the final salary scheme during the remedy period.

Before I start going into the details of this there are some parts which are not completely clear and so I must warn you that the figures may not give a true and accurate picture. However, the figures I do have are from an application made for retrospective AP. This date is asked for on the new application form in Section 2

I am going to assume that the “Pension Increase” will be applied from the date that the additional pension (AP), however this is not certain to be the case as the letter I have seen says this: “Your Additional Pension increases in value from the date of your full payment to your retirement date in line with pension increase factors.“

I am basing my assumption though on the fact that the payment requested does include an element of interest based on the time that has passed since the date asked for in Section 2 above. I don’t believe you can charge interest on something if you then take the date of the payment as the basis for applying the value of what has been bought.

Figures for 2016 – 50 Year Old

AP has to be bought in blocks of £250 but for the purposes of this post I will look at purchasing 4 such blocks, totalling £1,000. The date for this to be taken as 2016. I will also include the purchase of family benefits (50% to a partner etc)

£1,000 of FS AP (2016) would cost £16,080. Interest charged £1,382.

My Analysis

The interest for nearly 8 years is only 8.59%, that’s a simple annual interest rate of somewhere between 1.0% and 1.3%. That “feels” like good value.

Pension Increase: from 2016 to 2024 the inflation rate is in the region of 31.87%. If this is applied to the £1,000 then it would be worth £1,318.70 now.

Age to recover the investment

If the Pension Increase is applied from the elected date of purchase, which I believe it should, then dividing the cost (£17,462) by the current value (£1,318) gives us 13.3 years.

Taken at 60 that would be by 73.3.

If I am wrong about the way the PI is going to be added then it wold take 17.5 years to recover the investment, so by the age of 77.5

Compared to buying AP in the CA scheme now

The question here then, is it better to buy retrospective FS AP or to buy AP in the current career average (CA) scheme. For this comparison bear in mind that a 50 year-old in 2016 would now by 57/58.

A 57 year-old buying £1,000 of CA AP (2024) with family benefits would pay £15,160. That would take them 15.2 years to recover that investment. However, this AP would only be paid, in full, if they started taking it at 67.

67 plus 15.2 means they would get their investment back at the age of 82.2

I would suggest, therefore, that if you are considering the purchase of additional pension then it would be far better value to make an application for the retrospective purchase of AP from the remedy period than to buy it in the current career average scheme.

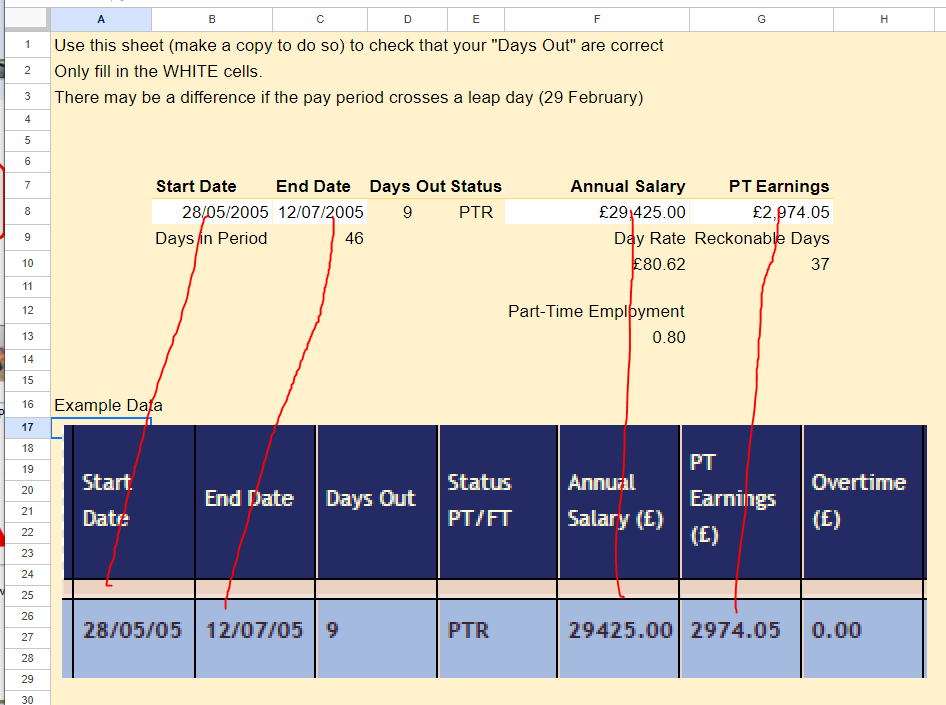

After fielding a number of queries regarding the days out and how they are recorded for part-time teachers I created this sheet to allow teachers to check their figures:

The way that part time work is recorded is not very intuitive and I sympathise with them. After all if you work 4 days a week then in a month you are likely to miss working on 4, or at the most 5, days in that month…so how come the statement shows 6 “days out”…there aren’t that many “Mondays” in ANY month!

To understand how part time service is recorded requires a different approach than just looking at the actual days you work in a week, we need to go much wider than that.

A full time teacher may work 5 days a week and they do that for 39 weeks in a year, that is 195 days, but their service record for a full academic year is recorded as all 365 days in the year (even in a leap year!)

In order for a part time worker to be credited with the correct proportion of the pension, i.e. 80% for one who works 4 days a week, that proportion is applied to each pay period. In a full academic year then a 0.8 part time teacher should get 0.8 x 365 days credited to their service record.

0.8 x 365 = 292 days. This is recorded by having the rest of the year, 73 days, labelled as “days out”.

If you have been in the TPS for LESS than 2 years you can transfer it to a private pension scheme. This calculator works out the transfer value (and it’s a lot more than getting a refund of your contributions!)

You have 12 months from starting, or re-entering, pensionable service to transfer other pensions in to the TPS. But is it worth it?

The value depends on two age;

Your age now

Your state pension age

This sheet will let you work out how much career average pension would be added if your transferred a lump sum from another private (defined contribution) scheme.

Ill-health retirement can now only be taken whilst in the career average scheme. This calculator, after you’ve made a copy of it, lets you put in your figures to see how much pension you would receive from each of the two tiers of ill-health retirement.

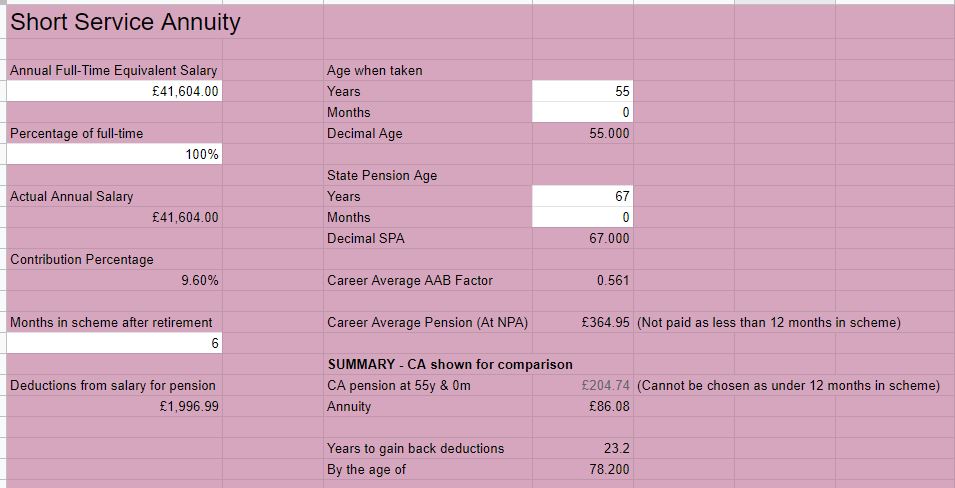

With the call going out to retired teachers to return to the classroom many have concerns about whether contributing to the pension scheme will give them value for money or not – particularly if they are going to be teaching for less than 1 year.

If they teach for more than a year then the career average scheme, that anyone who has already started taking their pension would be in on their return to teaching, normally pays back their contributions in under 10 years.

The pay back period for the short service annuity for anyone under 75 exceeds 13. So definitely not as good value as the actual pension.

One method (method B) used to calculate your final salary looks at your last 10 years salaries.

These are revalued using inflation, which often makes them worth more than you are currently earning!

When teachers have periods of pay freezes and below inflation pay rises this method often produces a better final salary pension calculation.

This spreadsheet will let you enter your last 10 year’s salary figures and to check what is going to happen over the next few months and years to your Final Salary Pension. If it is going to drop then you should seek advice on whether opting out would be appropriate.