Contracted Out

Up until 2016 Teachers were ‘contracted out’ of the additional state pension and so many do NOT qualify for the full NEW state pension…I explain.

Reflections on reaching for retirement

Contracted Out

Up until 2016 Teachers were ‘contracted out’ of the additional state pension and so many do NOT qualify for the full NEW state pension…I explain.

Very helpful video, that will save a lot of teachers a lot of time, and ensure they claim back their tax relief

If you retire at your Normal Pension Age and carry on, or return to, working then your pension may be abated (cut!).

Here I explain why and how to avoid it.

You want more?…

There are three ways to put more into your pension and to get more out of it. This presentation looks at the relative costs of Faster Accrual compared to Additional Pension.

One method (method B) used to calculate your final salary looks at your last 10 years salaries.

These are revalued using inflation, which often makes them worth more than you are currently earning!

When teachers have periods of pay freezes and below inflation pay rises this method often produces a better final salary pension calculation.

This spreadsheet will let you enter your last 10 year’s salary figures and to check what is going to happen over the next few months and years to your Final Salary Pension. If it is going to drop then you should seek advice on whether opting out would be appropriate.

Retiring next year, or in 30 years – the pay freeze could bomb your pension.

Fix it for £1

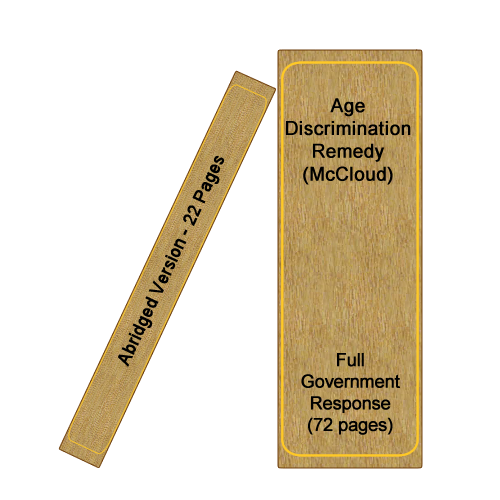

My abridged version of the Government’s response to the consultation on the removal of age discrimination in the public sector pension schemes.

For my own reference but I’m posting it as others may also find it useful. I have reduced it to the main points, focusing solely on the actions the Government is proposing to take.

I removed details on who responded to the consultation and the summaries of their contributions to boil it down to just what is proposed will happen without so much of the why it will happen.

The Full Proposal (72 pages)

The McCloud judgement declared that the transition of public sector pensions introduced in 2015 was illegal. This explains the relevance to the Teachers’ Pension schemes.

This spreadsheet looks at the kind of pension you can expect from the Career Average Scheme that everyone will be in from April 2022.

You enter how many years you are on each of the pay scales and it will, in today’s money, give you an estimate of the kind of pension you can expect at various ages – at 67 in full and also 62 and 57 if you were to take early retirement.

It also provides figures of what that service profile would have provided in the Final Salary schemes.

Is “Average” a dirty word, and is the Career Average Pension worth it?

Proudly powered by WordPress | Theme: Baskerville 2 by Anders Noren.